What does business insurance cover?

Business insurance can protect you and your assets against the everyday risks that come with running your business. Business insurance can cover you against things like professional mistakes, accidents, theft, damage and legal fees. Business insurance is important in the UK for limited liability companies, sole traders and self-employed people.

This page walks you through some of the types of business insurance that are available in the UK, with some pointers on the types of policies available.

Remember, this article is just an overview offering general information we are not advising you on which policies you should take out. It is also only relevant if you are in the UK. It doesn’t contain all the information you need to make your business insurance choices. You should always discuss your business activities with a registered insurance broker to help you get all the cover that you need. (Check the FCA website to make sure any broker you are thinking of using is registered.)

What types of business insurance should I get?

You will need to decide, with an insurance broker, which insurances best meet the needs of your particular business. There are various trade-specific packages, and also ‘commercial combined insurance’ which you can put together section by section based on what you actually need. These are often good value for money for small companies with no unusual types of risk.

Commercial combined insurance

Commercial combined insurance is designed to provide a wide range of insurance covers under a single policy. These policies bundle different covers together. They can be added or removed depending upon your particular business and circumstances.

Types of business insurance cover

First, let’s take a look at some of the main types of business insurance cover that are usually offered either as part of a package (commercial combined) or as separate policies.

They can be divided into three broad categories:

- Liability insurance can cover any damages you may have to pay, or the cost of rectifying mistakes you have made, as a result of your negligence; this could include property damage, injury or death

- Material damage insurance protects against damage, theft or loss of your business property and equipment

- Business interruption insurance is available for loss of income, or the increased cost of working if your business has to stop operating in its usual way due to a claim in category 2.

Insurance to cover your legal and compensation costs

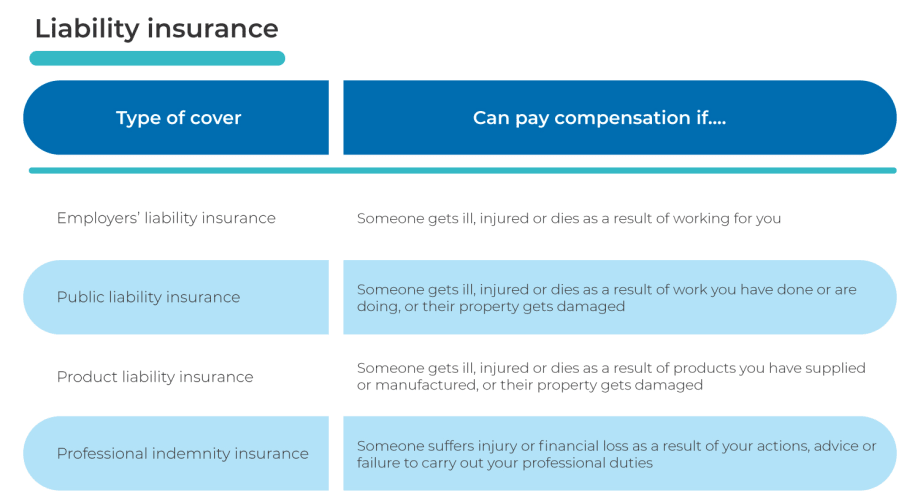

Employers’ liability insurance

Employers’ liability is a legal requirement for any UK business that has employees. It pays your legal costs and compensation payouts if your business is responsible for an employee getting ill, injured or killed as a result of working for you or your company. You are also responsible for harm to your employees caused by other employees, and employers’ liability insurance covers you for this too.

Payments can cover loss of earnings, future earnings, pain and suffering.

It covers you for claims made by past employees, too. If a former employee made a claim for compensation, you would file a claim with the insurer you were insured with while the incident happened. This may be a different company from your current insurer.

Public liability insurance

Public liability insurance covers compensation costs you could have to pay out as damages as a result of your negligence. This could include if someone dies, is injured or suffers damage to their property as a result of your business activities.

It’s designed to protect you financially against third party compensation claims. If a claim does become a legal matter, the policy may cover the cost of paying your lawyer in addition to any compensation you have to pay out.

For more on this type of insurance, visit the iCompario guide to Public Liability Insurance.

Product liability insurance

Product liability insurance is for faulty goods. It covers compensation payments if a product that you make or sell causes illness, injury, death or destruction of property to the person who bought it. You are sometimes, but not always, responsible for paying compensation even if the product wasn’t made by your business. You can be responsible even if you just handle the product. This means it can be a relevant type of business insurance policy for shop owners and online retailers and hauliers, for example, not just manufacturers.

For example, imagine the blade comes off a new knife handle and cuts someone’s hand when they are using it to slice a cake. This would probably lead to a claim that the knife was faulty. Cover in this case would include payment of compensation and any associated legal costs. It would not include the cost of replacing the defective knife itself.

iCompario spoke to one broker which had handled a surprising claim under product liability insurance. A haulier used to transport grain including barley, but for one customer was transporting sand to make up cement instead. They didn’t wash out the container before putting the sand in the container, meaning the cement that was finally made was contaminated with barley.

The story gets worse. The cement was used to build a flyover bridge which, being partly constructed out of barley grains, wasn’t really strong enough to take traffic. It had to be demolished and rebuilt.

A product liability claim was made against the supplier of the cement, whose insurer then made a subrogation (that means a claim made by an insurance company against anther insurance company) against the haulier, whose fault it really was because he had caused the contamination. The haulier’s insurer ultimately footed the bill under the category of public liability insurance.

This story involves two different types of business insurance which shows how important it is to have the full range of covers appropriate to your business.

About this website

iCompario is the free online marketplace for business products and services, where managers and owners can research and rapidly compare fuel cards, vehicle tracking systems, insurance, telecoms and other essentials. We follow up each online query by telephone, to make sure every site visitor finds their ideal, future-proof product at the best price possible.

iCompario is an IAR or Introducer Appointed Representative of business insurance broker Joseph W. Burley and Partners (UK) Ltd. which is registered with the Financial Conduct Authority.

Professional indemnity insurance

Professional indemnity insurance protects your customers from mistakes your business makes. If your business makes any money by offering customers advice, or a professional service a professional indemnity policy may be useful to you. It pays out the cost of rectifying your mistakes or compensating for financial losses you caused to others following your negligent advice. In this context, “negligent” can mean that you were being careless or that you made an honest mistake.

Each industry has its own unique risks and needs. These should be covered in their professional indemnity insurance. These policies tend to be specific to the trade or profession that you work in.

For example, a kitchen fitter advises and installs a ducting system over the hobs in a professional kitchen. After he has installed it, the restaurant owner finds the kitchen gets so hot it’s not safe for his chefs to work in the kitchen, so his restaurant cannot stay open. This was the fault of the kitchen fitter, who didn’t install a powerful enough extraction system. There’s no physical or “material” damage in this case, but there is a business that cannot operate, and makes a claim for loss of earnings against the kitchen fitter. The kitchen fitter has to pay compensation for losses. He would claim this from his own professional indemnity insurance.

Builders often give advice or draw up plans as well as doing the job. For instance, if a plumber recommended a certain type of boiler which then turned out to be inadequate to heat up the building, he might need to claim on his professional indemnity insurance to replace it with a suitable boiler.

For more on this type of insurance, visit the iCompario guide to Professional Indemnity Insurance.

Insurance to protect your business premises, stock and equipment

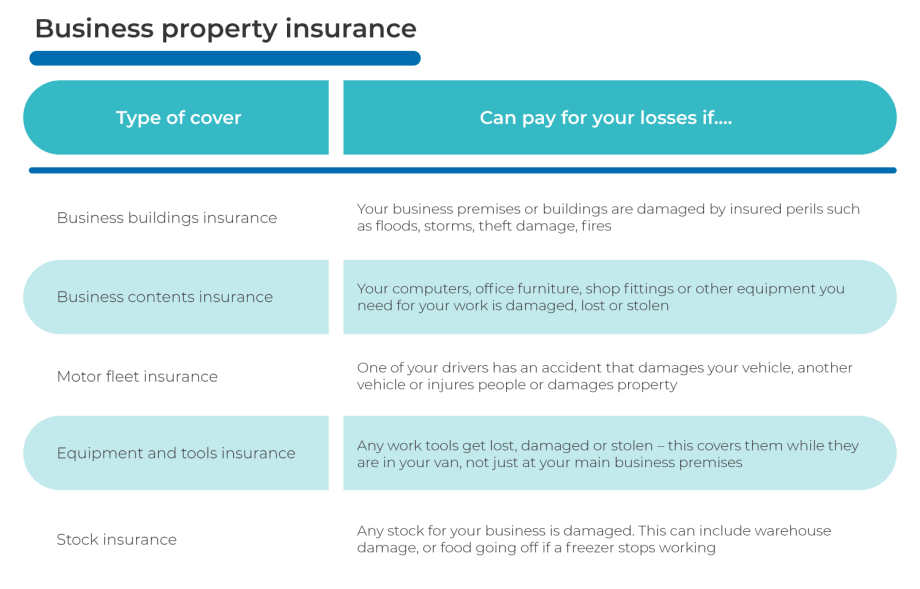

Business buildings insurance

Business buildings policies are very important if you conduct your business from any premises that belongs to your company. If you rent your business property from a landlord, it may be their responsibility to insure the building. If you are buying your business premises with a mortgage it is likely to be a condition of the mortgage that you have adequate buildings insurance.

Buildings insurance can cover a range of perils. Some types of damage, such as subsidence, may be opt-in or opt-out cover. It’s well worth taking the time to research thoroughly and make sure you get cover for exactly the perils you need. For example, if you manufacture weapons you will definitely need to make sure your fire and explosion clauses are watertight.

Large UK insurance company, Aviva, reported that 33% of its commercial property claims in 2019 were for water damage resulting from leaks, flooding or burst pipes and that this is typical most years. The second largest category of claims was for burglary damage at 11%, followed by accidental damage and storm damage both representing 8% of claims. Fire was the least common reason for claims at only 3%, however the size of damage in fires was usually very high.

The iCompario insurance team spotted one example of a large payout for a commercial fire in 2019. International insurer Allianz made a significant payment after someone put a lit sparkler into a dog poop dustbin. The burning dog mess got so out of hand that it set a nearby furniture shop on fire and the blaze destroyed the whole building.

Business contents insurance

Business contents insurance covers your equipment, machinery, computers, office furniture, fixtures and fittings whilst they are in your building. This type of insurance is useful to a lot of companies, whether or not they own their business premises.

About this website

iCompario is the free online marketplace for business products and services, where managers and owners can research and rapidly compare fuel cards, vehicle tracking systems, insurance, telecoms and other essentials. We follow up each online query by telephone, to make sure every site visitor finds their ideal, future-proof product at the best price possible.

iCompario is an IAR or Introducer Appointed Representative of business insurance broker Joseph W. Burley and Partners (UK) Ltd. which is registered with the Financial Conduct Authority.

Stock insurance

Stock insurance is useful for shops, restaurants and warehouses that have a lot of money invested in goods that are stored on their premises. It is also bought by a lot of companies that may hold stock for other businesses. This type of business insurance means you can claim up to a specified amount if stock is lost, damaged or stolen. If you are a manufacture, you need to insure not only your finished goods but also the raw materials you make them from.

Some insurers have restrictions on what they will cover. If you opt for stock insurance, it is important to check the finer details so you know what is excluded and what procedures you must follow. Insurers say that the main cause of claims being refused is because claimants did not follow the conditions that were part of the insurance contract.

For example, there could be a clause in a stock insurance policy that says you must keep food items in a locked freezer. If your stock is valuable you will probably need an alarm system installed.

Plant insurance

A plant policy, or contractors’ plant, can be a useful type of business insurance for contractors and tradesmen who use equipment away from their main premises. Builders, plumbers and many other professionals take expensive equipment to their places of work, and a plant policy means they can claim compensation if the equipment is lost, damaged or stolen.

It can also cover your legal liability under the terms of your hiring agreement to pay for loss or damage caused to hired-in plant and the cost of continuing hire charges.

Motor fleet insurance

‘Road Traffic Act Cover’ of your business vehicles – often called third party insurance – is compulsory, but you should consider cover for your own losses too with comprehensive insurance.

Rather than insuring individual vehicles with drivers specific to them, motor fleet insurance can cover all vehicles and drivers in a single policy. There are significant advantages to insuring business vehicles in this way, including cost savings, much less administration, and more flexibility.

Insurance to cover loss of income if something stops you working

Business interruption insurance

Business interruption insurance covers your loss of profit or increased working costs as a result of unforeseen insured events under the same policy. Business interruption insurance varies from one insurer to another. There is no standard business interruption wording. You need to check that what you are paying for meets your needs.

If an event, that is covered by your insurance, results in damage to your property and makes you lose income, business interruption insurance could cover you for at least some of the financial loss.

Business interruption cover follows the material damage section of your insurance rather than being a stand-alone cover. So, for example, if you needed to make a claim for damage from floods, fires or storms you could make a claim for business interruption as well if the original loss resulted in you losing profit or having to pay additional business costs.

Failure of supplies that you need to keep on manufacturing could also be covered. Sometimes you need to buy this cover separately. The most common extensions include losses resulting from:

- damage at the premises of suppliers

- damage at the premises of named customers

- damage to your property in transit

- access to your premises being prevented due to damage to nearby premises.

- prevention of access to your premises – in some insurance covers this includes the COVID-19 lockdown, and it may also include bomb threats

- damage at the premises of a public utilities

- the occurrence of a notifiable disease, vermin, defective sanitary arrangements, murder and suicide

iCompario tip:

You should discuss the way your business works with a business insurance broker to get all the insurance you need.

Cyber insurance

Cyber insurance can offer protection if your business is targeted by electronic criminals. It can cover you for loss of business, financial loss, liability and legal costs, public relations and communication with employees. This is an area where claims are growing rapidly, and the types of policy you can choose are improving all the time.

Even though cyber threats are increasing, insurers say the majority of payouts they make under this type of insurance are not as a result of attacks by third parties, but for damage relating to data systems that companies have inflicted on themselves by making mistakes.

Do I need business insurance?

The short answer is, yes. The real question here is to understand which types of business insurance will meet your specific needs.

Some types of insurance are compulsory in the UK.

If your business employs people in the UK, you are legally obliged to have employers’ liability insurance. There are some exceptions, however you should always check with an insurance broker to find out the latest regulations which may apply to you.

If you are buying your own business premises with a mortgage, your lender will insist that you have business buildings insurance.

The other types of business insurance you may need will partly depend on the size of your company and the kind of work you do.

In some cases, your customers might insist that you take out certain types of insurance.

iCompario tip:

You should use a business insurance broker to make sure you put together all the insurance your business activities need, and also to make sure you know the conditions you must follow to keep the insurance valid. There’s no point paying for insurance if you do not comply with the terms and conditions, and so end up making the insurance invalid.

Why you should get your business insurance through a broker

To get the right combination, iCompario strongly recommends that you use a broker for business insurance instead of trying to choose for yourself.

We all go to trade experts and professionals when we want a job well done. If we want an extension well built, we go to a reputable builder. If we want to get over an illness, we go to a doctor for their expert advice and generally avoid trying to figure out a remedy for ourselves.

No matter what job you do, you have specialist knowledge that you would never expect other people to be aware of. Similarly, for insurance you are likely to get much better results if you consult an expert broker on what you need, using the best insurance providers. DIY insurance can prove very costly in the long run.

A business insurance broker should help with a personalised assessment of the business risks you need to cover, and offer advice on the right types of business insurance policies for you. If you are starting out with a new business, there may be types of insurance you didn’t know were available or necessary.

You should also review your insurances with a good broker each year, to make sure nothing gets overlooked as your business grows and evolves.

Major UK insurer Aviva explains the main reason why insurance claims are refused.

‘This may be because the customer has not bought the right level of cover, they’ve misunderstood the cover they have bought, or they have not complied with the terms that have been agreed with us, such as switching the intruder or fire alarm on when they leave the business premises.

‘We know that commercial insurance can be complex, so we work constantly to make it as easy as possible, including creating clear and simple policy wording and working with our 2,300 brokers to make customers aware of the risks of not having the right level of cover. Our advice to any business with more complex insurance needs is that they speak to their broker to make sure they have the right cover and fully understand what their policy provides.’

In some cases, your customers might insist that you take out certain types of insurance.

iCompario tip:

Good brokers ask lots of questions to make sure they understand your business properly. They should never make assumptions. If a broker isn’t asking you detailed questions, they may not be getting the full picture they need to obtain the most suitable insurance policies for you that meet all your needs. If you use a broker who takes a bit of a “one size fits all” approach, you may be wasting money on extra insurance cover that isn’t really relevant to your business. Insurance brokers who go to insurers with lots of detail are often offered better prices. This is because they present you, the client, in a clearer way to insurers with no hidden surprises – which is just the type of client insurance companies want.

About this website

iCompario is the free online marketplace for business products and services, where managers and owners can research and rapidly compare fuel cards, vehicle tracking systems, insurance, telecoms and other essentials. We follow up each online query by telephone, to make sure every site visitor finds their ideal, future-proof product at the best price possible.

iCompario is an IAR or Introducer Appointed Representative of business insurance broker Joseph W. Burley and Partners (UK) Ltd. which is registered with the Financial Conduct Authority.

About this website

iCompario is the free online marketplace for business products and services, where managers and owners can research and rapidly compare fuel cards, vehicle tracking systems, insurance, telecoms and other essentials. We follow up each online query by telephone, to make sure every site visitor finds their ideal, future-proof product at the best price possible.

iCompario is an IAR or Introducer Appointed Representative of business insurance broker Joseph W. Burley and Partners (UK) Ltd. which is registered with the Financial Conduct Authority.

Sources and further reading

For information on insurance and the insurance industry, visit The Chartered Insurance Institute.

To check of an insurance broker you are thinking of using is legally registered, look them up on the The Financial Conduct Authority website.

Keep up to date with your legal obligations as an employer by visiting the UK government website on Employers’ liability insurance.

For an overview of your obligations to comply with the UK law on product safety, see the government website Product Safety Advice for Businesses.

For an overview of cybercrime risks and insurance, visit Wikipedia ‘Cybercrime’ and Wikipedia ‘Cyber Insurance’.